January 10, 2022

Perpetual: inside the business of funds management

This analysis of Perpetual is part of Equity Mates Summer Series, proudly supported by Superhero. Listen to the podcast episode here with CEO Rob Adams. In brief Perpetual Limited is a publicly owned investment manager which offers a range of financial products and services in Australia. Equity Mates take The funds management industry can be…

By Superhero Team

Scan this article:

This analysis of Perpetual is part of Equity Mates Summer Series, proudly supported by Superhero. Listen to the podcast episode here with CEO Rob Adams.

In brief

Perpetual Limited is a publicly owned investment manager which offers a range of financial products and services in Australia.

Equity Mates take

The funds management industry can be difficult to understand. There are some big names with hundreds of billions or trillions of dollars under management, and it can be difficult to piece it all together. Here’s how we conceptualise it.

There are big pockets of money around the world – endowments, pension funds (including superannuation), sovereign wealth funds, family offices, high net worth individuals etc. There are thousands of fund managers that have started to service these big pockets of money and manage it on their behalf. These are some of the names you might be familiar with – Platinum, Magellan, Perpetual, Janus Henderson, Vanguard, Blackrock etc.

Within these thousands of fund managers, there are a number of different specialities. There are venture capitalists (Andressen Horowitz, Sequoia, Blackbird, Airtree), private equity (Blackstone, KKR, Carlyle), index investing aka passive (Vanguard, Blackrock, State Street, Betashares), property (Dexus, Charter Hall, Goodman Group), bonds and fixed income (PIMCO, First Sentier). One of these specialities is public equities (aka stock market) investing and that includes names like Magellan, Platinum and Perpetual.

The name of the game for Perpetual, or any of those names, is to secure more money to manage from the endowments, pension funds, sovereign wealth funds, family offices and high net worth individuals. The more money they manage, the more they can collect in fees. Right now, Perpetual manage ~$100 billion. The question for investors is, how big can that number get?

Tell me about Perpetual

Perpetual is one of Australia’s oldest companies, being founded in 1886. It is one of Australia’s largest wealth managers with almost $100 billion in assets under management. It is also an expert adviser to high net worth individuals, families and businesses and a leading provider of corporate trustee services.

Asset managers make money in two key ways. Firstly, management fees, charged as a percentage of assets under management. Secondly, performance fees, additional fees charged on any outperformance a fund manager achieves over a set benchmark (for example, if the benchmark is the ASX200 and it returns 5% and the fund manager returns 15%, they may charge an additional fee on the 10% of outperformance).

Ultimately, for a fund manager, the business model is pretty simple. Convince more people, organisations and businesses to have you manage their assets (increases management fee) and invest it as well as possible (to increase your performance fee). The model is easy to understand, the hard part is doing it.

What about the industry?

A key reason why it is so hard to execute, is that there are so many people trying to do it.

Funds management is an incredibly crowded space. In Australia alone, there are over 3,700 funds on offer. And as it gets easier to invest overseas, fund managers are also competing with all of their overseas rivals as well.

Australia’s managed funds industry is large, the 5th largest in the world, largely thanks to our superannuation system. In March 2021, the Australian managed funds industry held $2.5 trillion in assets.

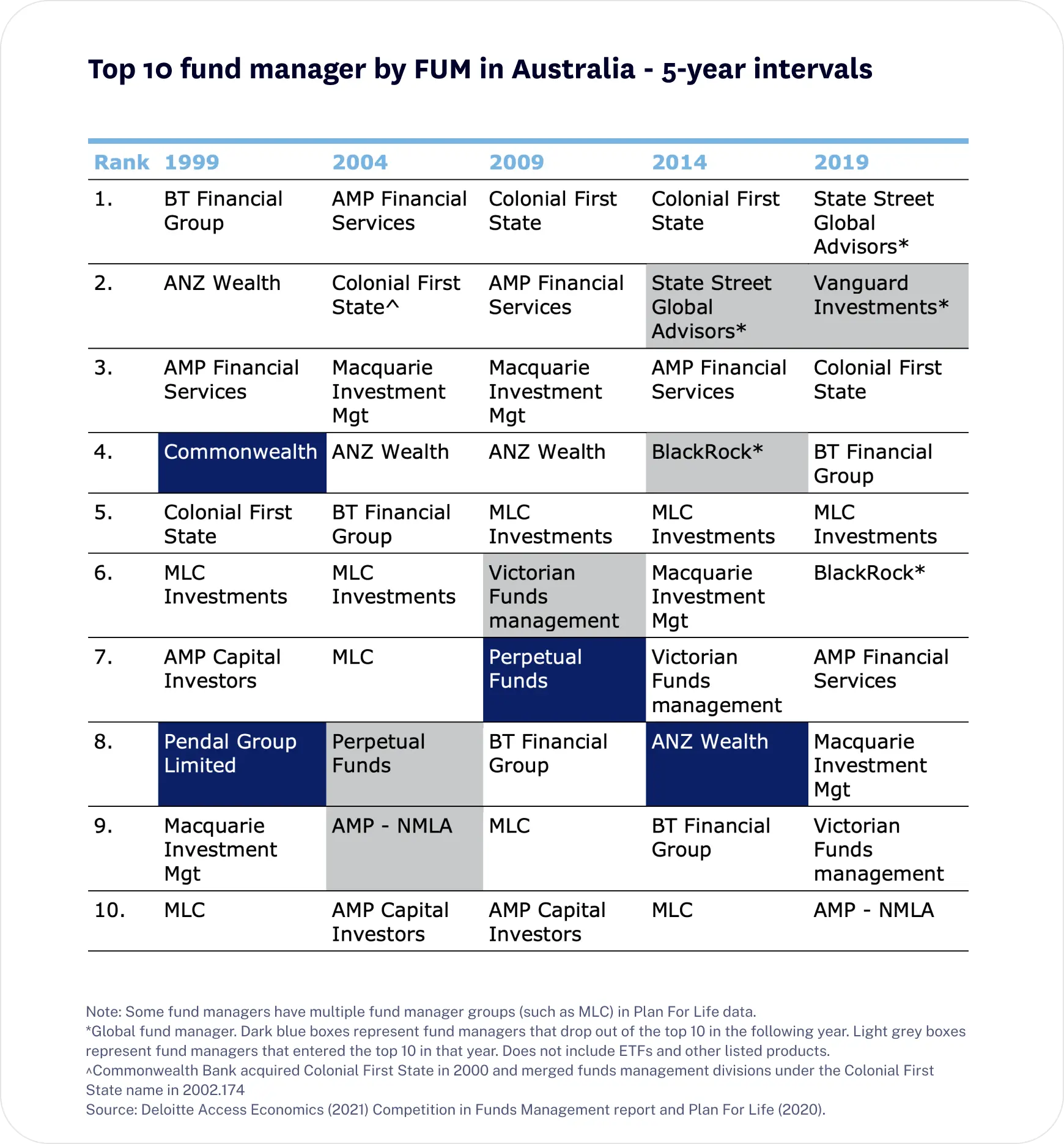

While there is a lot of competition in the industry, the majority of the assets accrue to the top. The largest 10 fund managers hold more than 50% of the assets under management in Australia. The top 10 shifts over time, see the table below, but many of the names remain the same.

Let’s get to the numbers

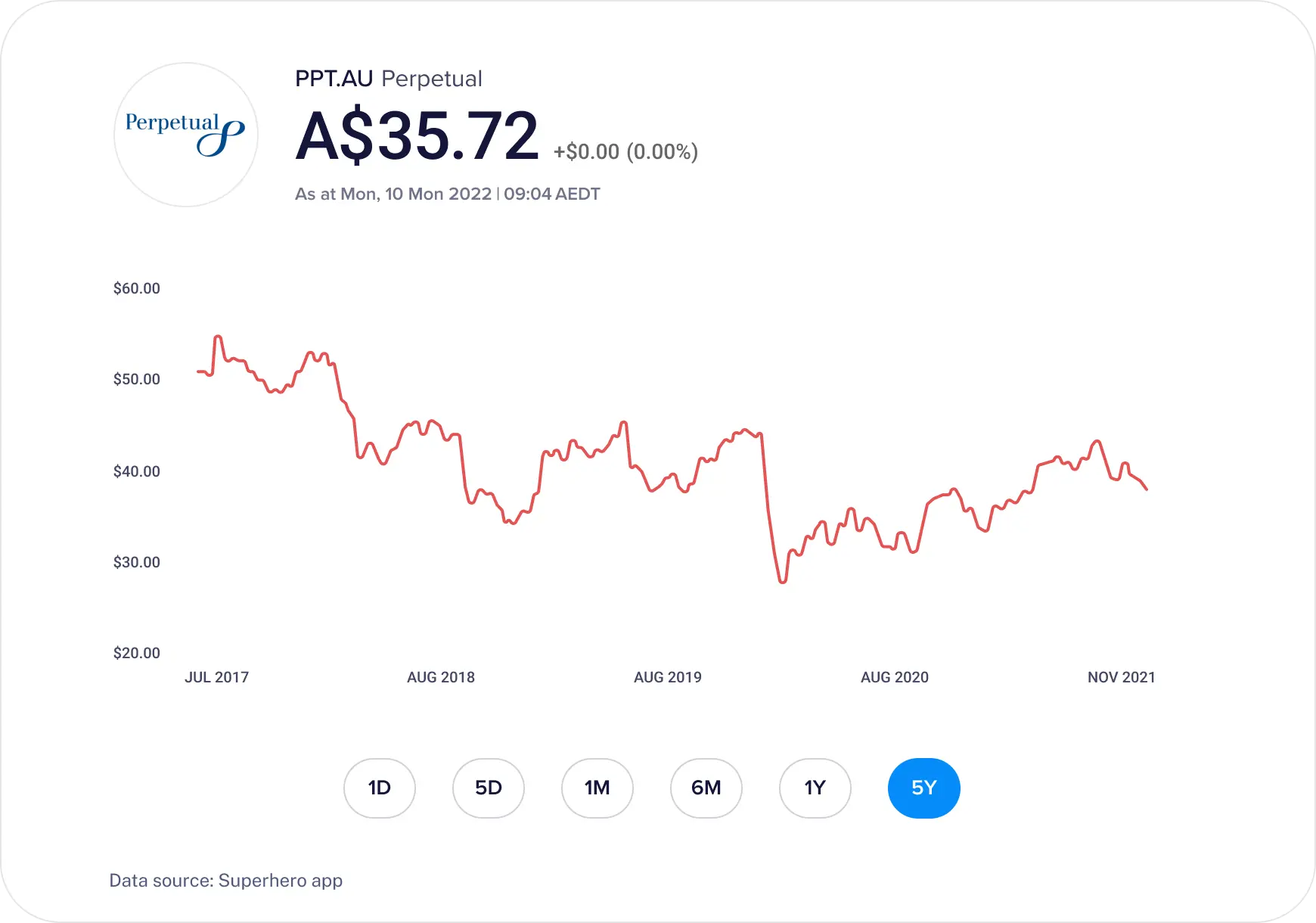

Share price

Between 1999 and 2008, Perpetual quadrupled in value. Then in the last 10 years, it has basically traded flat. I guess when you have a 140 year history you have to zoom out a little. Over the past 5 years, the share price is down 24%.

Perpetual isn’t going to be a growth stock but they do currently have a 5% dividend yield. So keep in mind the total return of any of these stocks.

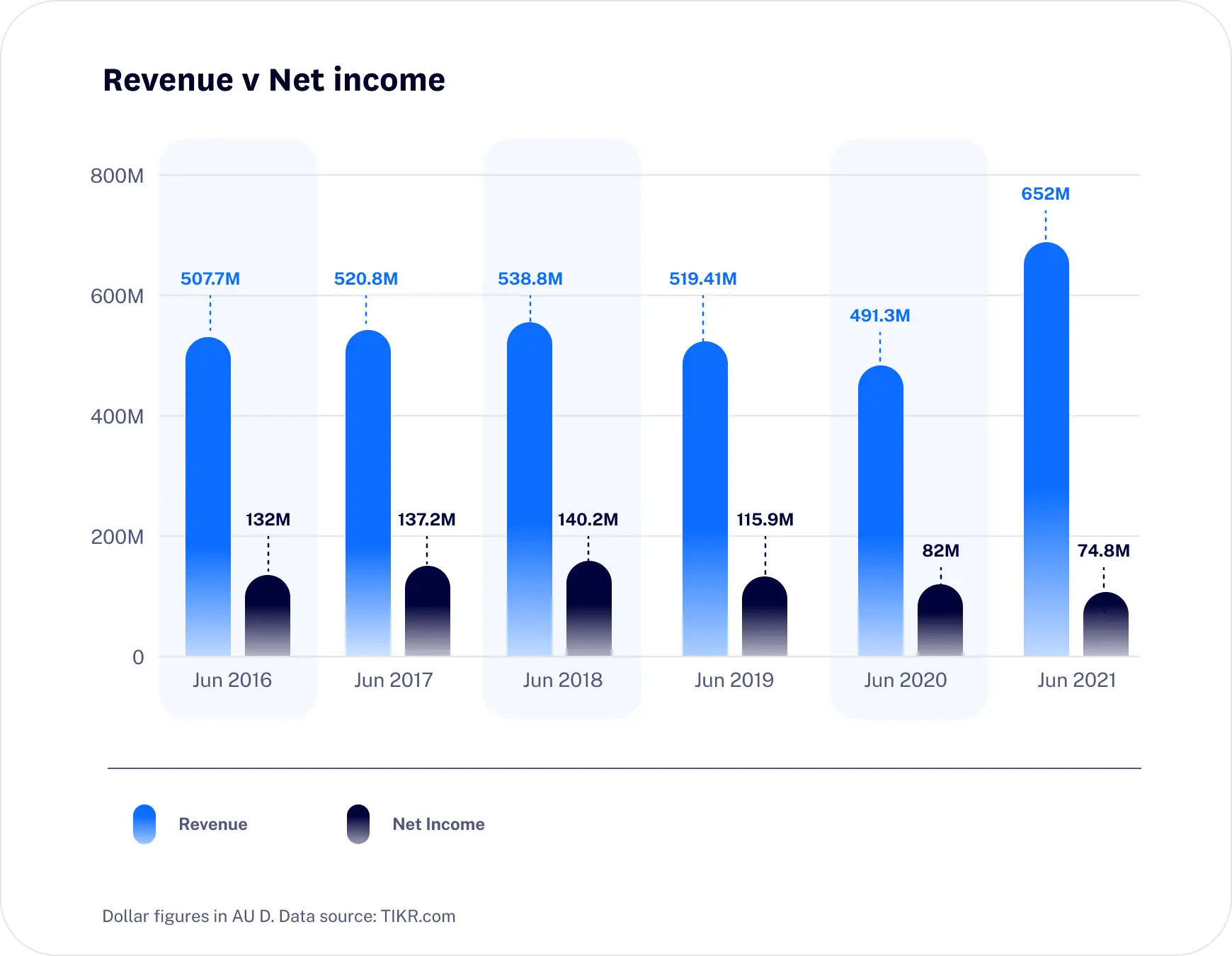

Revenue and profit

Outside of the 2021 financial year, Perpetual’s revenue has remained relatively stable, coming in around the half a billion dollar ($500m) mark every year. What is noticeable is that between FY18 and FY21 the company’s profit halved – from $140 million down to $75 million.

Final thoughts on Perpetual

Funds management can be one of the most lucrative businesses globally. When things are going well, the market has confidence in your abilities, and more and more investors are committing funds, you can do no wrong. However, on the other side, if you underperform and the market loses confidence it isn’t hard for investors to pull their money and go to another fund manager.

Despite this, Perpetual seems to have put together an incredibly steady track record. Not too much growth – in the 2005 financial year they earned $342 million in revenue – but not a big fall either. The company has been around for 140 years and wants to be around for the next 140, and as a potential investor, it is important to take a very long term time horizon when assessing this company.

Become a part of

our investors' community

Why you should join us:

- Join free and invest with no monthly account fees.

- Fund your account in real time with PayID.

- Get investing with brokerage from $2. Other fees may apply for U.S. shares.

Read our latest articles

Make knowledge your superpower and up your skills and know-how with our news, educational tools and resources.